If you are building an app that accepts crypto, such as a DeFi protocol, a gaming platform, a marketplace, or an exchange, the payment layer is the part that either works seamlessly or kills your conversion funnel. Web3 payments have matured well beyond "paste a wallet address and hope for the best." In 2026, the infrastructure exists to accept deposits from any token on any chain, with bridging, gas, and swapping handled automatically in the background.

This guide walks through what web3 payments are, what solutions are available, and how to integrate cross-chain deposit infrastructure into your application step-by-step.

What Are Web3 Payments?

Web3 payments are financial transactions settled directly between digital wallets on blockchain infrastructure, without banks, card networks, or traditional payment processors as intermediaries. Where a conventional payment flows through a chain of middlemen: an acquirer, card network, issuing bank, each taking a cut and adding latency. A Web3 payment solution moves value directly from sender to recipient on-chain.

The basic flow works like this: a user connects their wallet to your app, your app presents a payment or deposit request, the user signs a transaction, the blockchain confirms and settles it, and the funds arrive at the destination (whether that's your wallet, your treasury, or a smart contract). Settlement happens in seconds to minutes, not the 1–3 business days typical of ACH or wire transfers. And it works 24/7, globally, with no bank holidays.

Web3 payments take several forms in practice:

- Cryptocurrency payments: BTC, ETH, or other native tokens are the original use case.

- Stablecoin payments: USDC and USDT have become the dominant form for commerce, removing price volatility from the equation.

- Tokenized asset transfers: Loyalty points, in-game currencies, and real-world asset tokens are an emerging category with their own set of infrastructure needs.

The use cases developers are building on these rails today span a wide range: DeFi deposits into lending protocols and yield vaults, NFT purchases, in-game item sales, subscription services paid in crypto, cross-border payroll, and creator monetization. The common thread is that the payment settles on-chain, without a bank in the middle.

What Are Web3 Payment Solutions?

Web3 payment solutions are implemented by integrating the right set of infrastructure tools. SDKs, APIs, widgets, and platforms that abstract the complexity of accepting on-chain payments so you don't have to build everything from scratch. They handle the plumbing: wallet connectivity, transaction construction, on-chain execution, confirmation callbacks, and optionally fiat conversion.

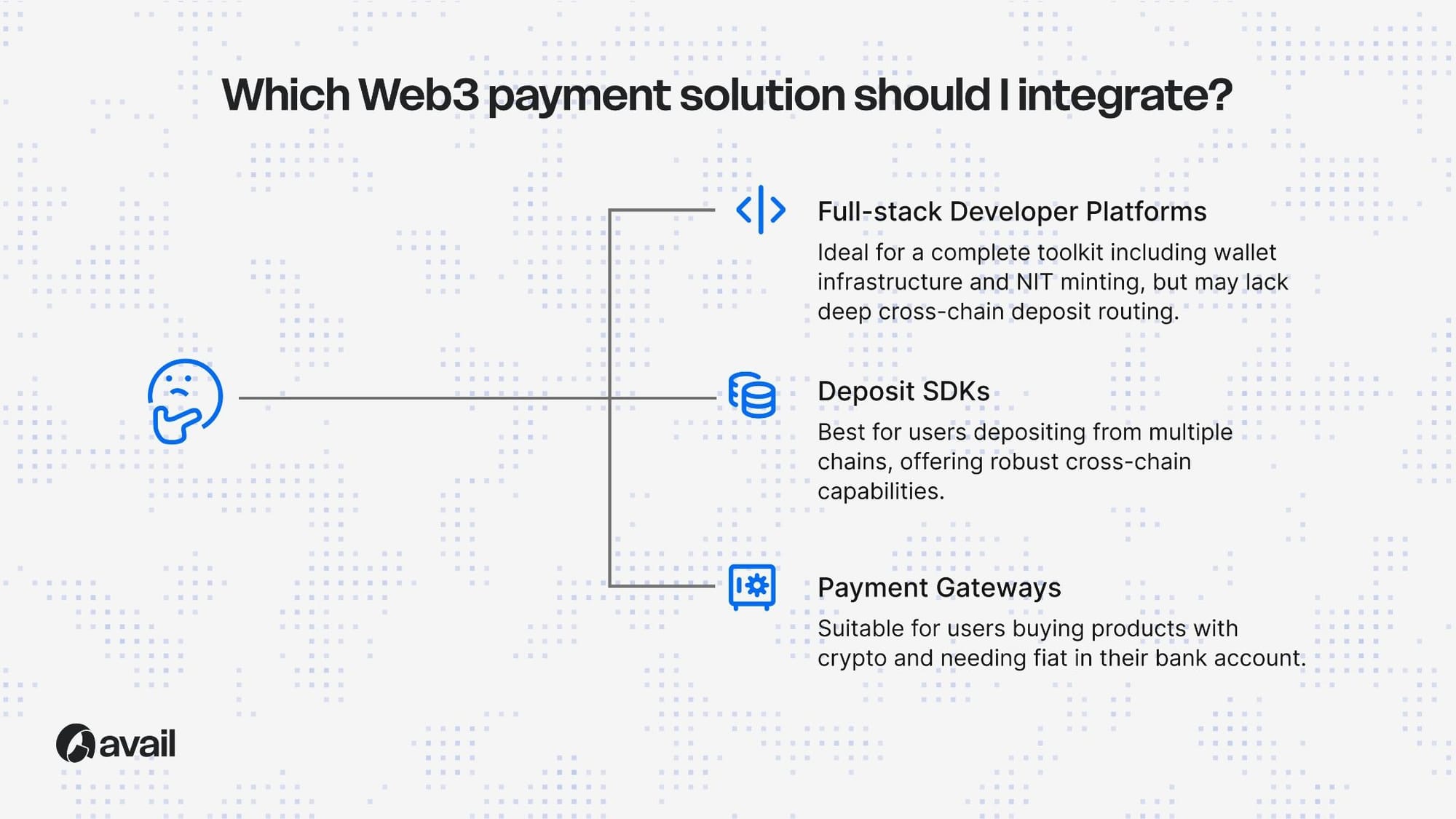

These solutions fall into three broad categories, each suited to different use cases.

- Payment gateways like BitPay, Coinbase Commerce, and NOWPayments are the closest analogues to traditional payment processors. They are designed for merchant checkout flows: a customer pays in crypto, the gateway converts it to fiat, and the merchant receives dollars in their bank account. They offer plugins for Shopify and WooCommerce, invoicing tools, and compliance features. If you are running an e-commerce store and need fiat settlement, this is your category. For a full comparison of these options, see our guide to the best cryptocurrency payment gateways in 2026.

- Deposit SDKs solve a different problem. They are built for apps where the "payment" is deposited into a smart contract, such as a vault, a lending pool, or a perpetual exchange margin account. Instead of converting crypto to fiat, they route assets from any source chain to the target contract, handling cross-chain bridging, token swapping, and gas abstraction automatically. Avail Deposits, built on the Avail Nexus SDK, is the primary example in this category.

- Full-stack developer platforms like Thirdweb, Moralis, and Sequence bundle payment capabilities alongside broader tooling for wallet infrastructure, NFT minting, and game economy management. They are useful if you need a complete development toolkit, though they typically don't go as deep on cross-chain deposit routing as purpose-built deposit SDKs.

Make an impactful choice based on your requirements. If your users are depositing into smart contracts from multiple chains, you need a deposit SDK. If they are buying products with crypto and you want fiat in your bank, then you need a payment gateway.

Benefits of Integrating Web3 Payments

Before getting into implementation, it's worth understanding why web3 payments are worth the integration effort in the first place. The benefits are practical, not theoretical.

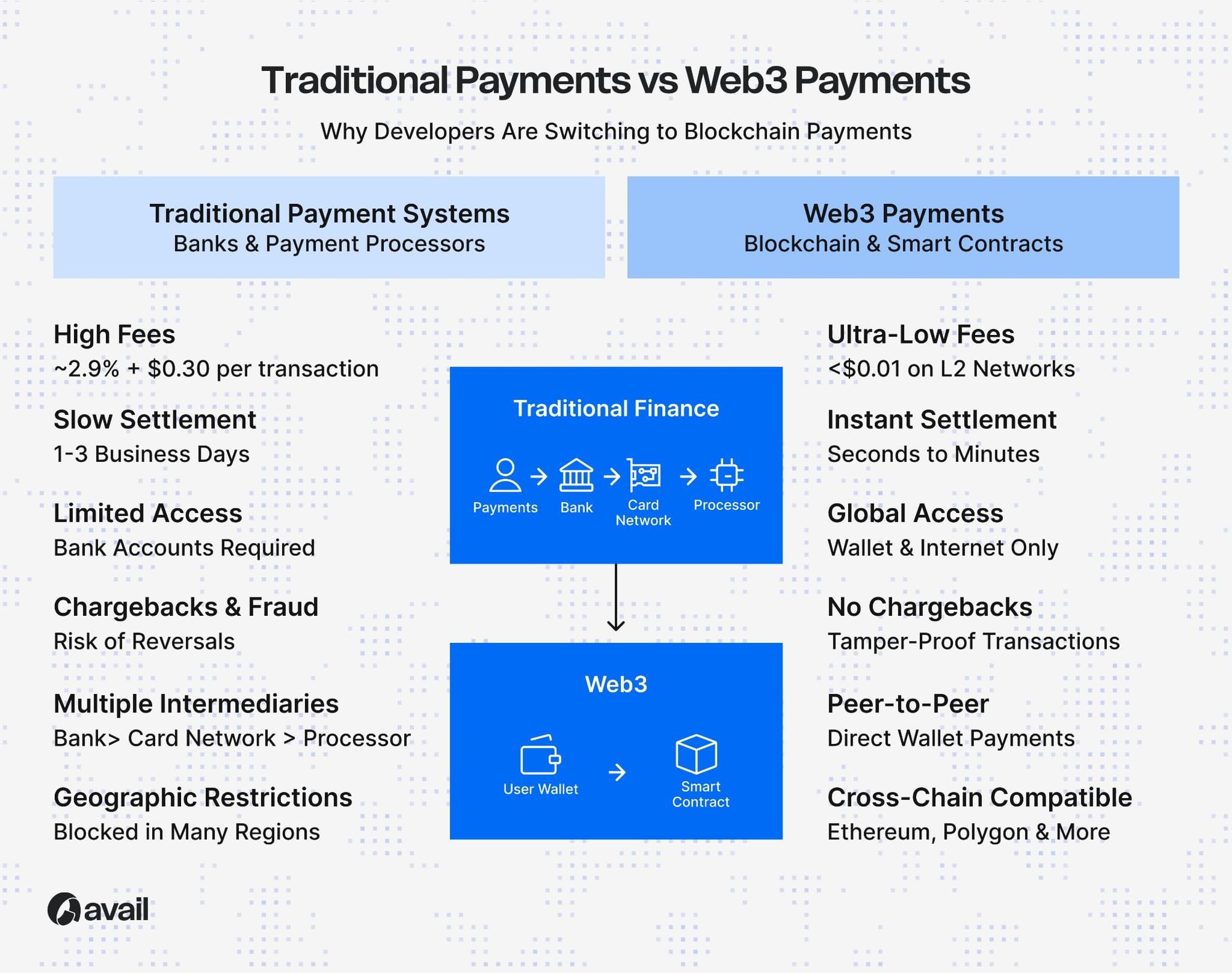

Lower transaction fees: Traditional card processing through Stripe or PayPal typically costs 2.9% plus $0.30 per transaction. Stablecoin payments on Layer 2 networks like Base or Arbitrum cost a fraction of a cent in gas fees. Even accounting for cross-chain routing overhead, the economics are significantly better, especially at scale.

Faster settlement: ACH transfers take 1–3 business days. International wires can take longer. Crypto transactions settle in seconds to minutes, depending on the chain, and funds are immediately usable by the recipient. No holds, no pending periods, no business-day dependency.

Global access without borders: According to the World Bank's 2025 Global Findex report, approximately 1.3 billion adults worldwide remain unbanked. Web3 payments require no bank account, just a wallet and an internet connection. Your app becomes accessible to anyone, anywhere, 24/7.

Enhanced security: Every transaction is verified by cryptographic signatures and settled on a tamper-proof public ledger. Non-custodial payment flows mean you never hold user funds; they move directly from the user's wallet to your contract.

Transparency and auditability: Every transaction is recorded on-chain, publicly verifiable in real time. This replaces manual reconciliation with programmatic verification and simplifies compliance and auditing.

New monetization models: Web3 rails enable business models that traditional payments can't support. Innovative mechanisms like token-gated access to premium content, on-chain subscriptions with programmable billing, yield-generating deposit flows, and revenue-sharing via smart contracts are all possible.

Expanded user base across chains: This is the benefit unique to cross-chain solutions. Single-chain payment integrations limit you to users on that specific network. Cross-chain solutions let you accept payments from users on Ethereum, Arbitrum, Optimism, Base, Polygon, and more, dramatically expanding your addressable user pool without per-chain integration work.

The Cross-Chain Challenge: Why Most Integrations Break

Here's where most web3 payment guides stop. They explain the benefits, show you how to connect a wallet, and call it done. But in practice, the hardest problem in web3 payments isn't accepting a payment; it's accepting a payment from a user whose assets are on the wrong chain.

The reality of 2026 is that user funds are scattered. A typical DeFi user might hold USDC on Arbitrum from a recent trade, ETH on Ethereum mainnet from an older position, USDT on Polygon from a friend's payment, and some tokens on Base from an airdrop. When they open your app and want to deposit, the odds that their assets are already on the right chain, in the right token, are slim.

Most web3 payment solutions don't handle this. They assume the user is connected to the correct network with sufficient balance in the expected token. When that assumption fails, and it usually does, the user is on their own. The resulting flow looks something like this: the user realizes their assets are on the wrong chain, leaves your app to find a bridge, approves the bridge transaction, waits for confirmation, switches networks in their wallet, returns to your app, reconnects, approves the deposit token, and finally completes the deposit. That's a 10-step process that can take 10–20 minutes or more. Each step is a place where users give up and leave.

This isn't a niche problem. Stablecoin transaction volumes hit $33 trillion in 2025, according to Artemis Analytics, and that volume is spread across dozens of chains, not concentrated on one. The cross-chain movement of assets is the norm, not the exception.

For developers, the fragmentation problem is just as painful. Supporting multiple chains means maintaining separate deployments, writing gas estimation logic per chain, managing token approval flows per network, and integrating bridges individually. Every new chain you want to support multiplies your maintenance surface. It's engineering time spent on infrastructure plumbing instead of your actual product.

Traditional payment gateways don't solve this; they were designed for single-chain fiat conversion, not multi-chain on-chain routing. Broader developer platforms address wallet connectivity but don't handle deep cross-chain deposit aggregation with solver-based routing and gas abstraction.

This is the exact gap that Avail Deposits fills. It collapses the entire multi-step, multi-chain deposit flow into a single user action: click deposit, confirm once, done. Bridging, swapping, gas, and routing are all handled under the hood by a competitive solver network.

How to Enable Web3 Payments for Your App or Website

Here's the practical, step-by-step path from zero to accepting cross-chain web3 payments.

Step 1: Choose Your Payment Approach

You have three paths, and the right one depends on your use case.

If you are building an e-commerce store or SaaS product and want to receive fiat in your bank account, a payment gateway like BitPay, Coinbase Commerce, or NOWPayments is the right fit. Install their plugin or integrate their API.

If you are building a DeFi protocol, on-chain game, or crypto-native app where users deposit into smart contracts, a cross-chain deposit SDK gives you the best balance of chain coverage, user experience, and integration speed. This is where Avail Nexus fits.

Step 2: Evaluate Cross-Chain Support, Fees, Security, and UX

Before committing to a solution, evaluate it against the criteria that matter most: chain coverage (15+ EVM chains vs. 2–3), gas abstraction (full vs. users need native tokens), security model (non-custodial, audited smart contracts), token support (any-token-in vs. limited pairs), and integration effort (1-line widget vs. weeks of per-chain work). Our payment gateways comparison covers these criteria in detail.

If you have highly specialized requirements and dedicated engineering resources, a custom build gives you maximum control at the cost of significant development and maintenance effort.

For most crypto-native apps, the deposit SDK path delivers the highest impact with the lowest integration overhead. Let’s see how to integrate that.

Step 3: Integrate Avail Deposits (Nexus SDK)

The simplest integration path is the drop-in widget. Install the SDK package and embed the component in your frontend. Check details here.

That's the minimum viable integration. The widget handles wallet connection, chain detection, balance aggregation across all supported chains, route optimization through the solver network, and transaction execution. The user sees a clean deposit interface; the complexity is invisible.

For developers who want full control over the UI, the Nexus SDK exposes a programmatic API with deposit flow methods, webhook callbacks, and event listeners. The SDK deep-dive on the Avail blog covers the full API surface and advanced integration patterns.

Select which source chains your app will accept deposits from. Configure the destination chain and target token, and set any application-specific parameters like minimum deposit amounts or token whitelists. Deploy your integration to a supported testnet. Verify end-to-end deposit flows from multiple source chains and token types. Test edge cases: what happens when a user has insufficient balance, when they attempt to deposit an unsupported token, or when network conditions create routing delays. If you are using the programmatic API, verify webhook callbacks and receipt handling.

Step 4: Go Live and Monitor

Push to production and monitor deposit flows through the SDK's built-in analytics. Track conversion rates, settlement times, and source chain distribution to understand where your users are coming from.

Apps like QuickSwap, Clober, and Bean Exchange use this approach to eliminate deposit friction.

Challenges of Web3 Payments and How to Overcome Them

Web3 payments aren't without friction points. Here are the most common challenges developers face and how to address each one.

Price volatility: Crypto prices fluctuate, which makes accepting volatile tokens risky for merchants and confusing for users. The fix: support stablecoins (USDC, USDT) as your default payment or deposit token. Avail's any-token-in routing handles this neatly. A user can pay with whatever token they hold, and the solver network automatically converts it to the stablecoin your contract expects.

Regulatory compliance: Crypto payment regulations vary by jurisdiction and are still evolving. Non-custodial architectures reduce your regulatory surface area because you never hold user funds; they flow directly from wallet to contract. If your jurisdiction requires KYC/AML, layer it on top at the application level rather than depending on the payment infrastructure to enforce it.

Security risks: Smart contract vulnerabilities, bridge exploits, and phishing attacks are real threats. Use audited, non-custodial infrastructure. Avail Deposits routes through audited smart contracts.

UX complexity: The biggest barrier to web3 payment adoption is still UX. Users shouldn't need to understand bridging, gas tokens, or network switching. The best web3 payment flows abstract all of this away. The user sees one balance and clicks one button. Full gas abstraction, where users never need native tokens on any chain, is essential for a mainstream-quality experience.

Cross-chain fragmentation: Instead of building and maintaining separate integrations for each chain, use a single SDK that handles routing, bridging, and swapping under the hood. This is the core value proposition of cross-chain deposit infrastructure and the reason a single integration through Avail Nexus can replace weeks of per-chain plumbing.

Frequently Asked Questions

How do I add crypto payments to my website?

Choose a web3 payment solution that fits your use case: a payment gateway for e-commerce (BitPay, Coinbase Commerce) or a deposit SDK for on-chain apps (Avail Nexus). Integrate it into your frontend via plugin, API, or widget. For cross-chain deposits from any token on any of the top EVM chains, the Avail Nexus SDK can be integrated.

How do I integrate payment into my website?

For traditional crypto payments, use a payment gateway like BitPay or Coinbase Commerce. They offer plugins for Shopify, WooCommerce, and other platforms. For cross-chain web3 payments where users deposit into smart contracts, integrate the Avail Deposits SDK. It handles bridging, gas, and swaps automatically across all major EVM chains.

How to activate Web3?

Web3 isn't a toggle; it's an integration layer. To add web3 functionality to your app, connect a wallet provider (WalletConnect or similar), integrate a payment or deposit SDK like Avail Nexus, and configure your smart contract interactions.

What is Web3 payment?

A web3 payment is a financial transaction powered by blockchain technology, settled directly between digital wallets without banks or payment processors in the middle. Web3 payments use cryptocurrencies, stablecoins, or tokenized assets, and are transparent (recorded on a public ledger), fast (seconds to minutes), and globally accessible (no bank account required).

What is the best web3 payment solution for developers?

It depends on your use case. For single-chain e-commerce checkout with fiat settlement: Coinbase Commerce or NOWPayments. For cross-chain DeFi deposits across popular EVM chains with automatic bridging, gas abstraction, and any-token-in support: Avail Deposits via the Nexus SDK. See our full comparison of cryptocurrency payment gateways for a detailed breakdown.